Supply and Demand: Short Domain Names Investment Case Study

Supply and Demand: Short Domain Names Investment Case Study

Why might short .com domain names make a good investment? The answer comes down to supply and demand — one of the most fundamental principles in economics and the backbone of any market economy. This case study applies that principle directly to the domain name market, using the November 2, 2007 four-letter .com buyout as a real-world example.

Real Estate vs. Virtual Real Estate

Domain investing mirrors real estate investing in several important ways. In the physical world, a prime property like the Bank of America Tower commands enormous prices — and the virtual equivalent, a premium one-word .com, requires the same kind of capital. That tier is out of reach for most investors.

The more accessible segment is the lower end of real property compared to four-letter .com domains. A four-letter .com is relatively cheaper and something an individual investor can actually own and manage.

The parallels run deeper. When buying physical real estate, the rule is location, location, location. When buying domains, the rule is short, shorter, shortest. And just as you should not buy a house in the desert, you should not buy a domain with dashes or numbers in it — those are the deserts of the domain world.

Risk factors also mirror each other. Real estate faces earthquakes, floods, and the theoretical possibility that humanity moves off-planet. Domains face competition from new extensions — .net, .org, .io, .ai, and the hundreds of new gTLDs that have launched since 2012. You can now register a .anything, and some speculate that traditional domains might eventually lose relevance entirely. Whether you invest depends on your assessment of those risks and your confidence in the fundamentals.

The Mathematics of Supply

The supply side of four-letter .com domains is governed by simple combinatorics. Each position in a four-letter domain can hold one of 26 letters. The total number of possible combinations is 26 × 26 × 26 × 26 = 456,976. That is the absolute ceiling — no more four-letter .com domains can ever be created.

For three-letter .coms, the number is even smaller: 26 × 26 × 26 = 17,576.

At any given time, each of those 456,976 four-letter domains is in one of three states: freely available to register, held by a domain investor (domainer), or held by an end user (a business actually using the domain). The long-term trend is clear: end users acquire domains from domainers, and freely available domains get registered. Both movements shrink the available supply.

This supply can only move in one direction — down. A domain that gets purchased by a business operating a website is unlikely to ever return to the open market. The pool of acquirable four-letter .coms contracts year after year.

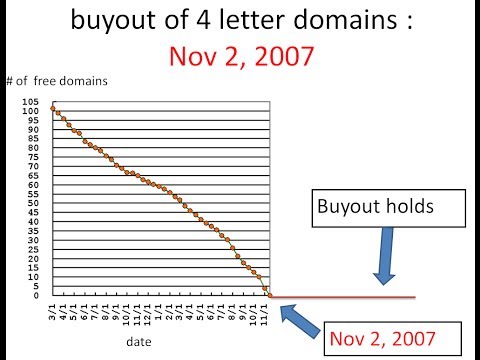

The November 2, 2007 Buyout

November 2, 2007 was a landmark date in the four-letter .com market. On that day, the number of freely available (unregistered) four-letter .com domains hit zero. Every single combination from AAAA.com through ZZZZ.com was registered. If you wanted a four-letter .com after that date, you had to buy one from an existing owner.

Looking at the data leading up to that date tells a dramatic story. A chart of freely available four-letter .coms over time shows a steady decline, then a sharp drop as speculators and investors rushed to register the remaining names. By November 2, the line hit the x-axis. The buyout was complete.

Anyone who invested before the buyout date was rewarded. But even after the buyout, opportunities remained. Some investors doubted whether the buyout would hold — whether names would expire and become available again. That uncertainty kept prices below where fundamentals suggested they should be. So far, the buyout has held.

Letter Quality and Pricing

Not all four-letter .com domains are equal. The letters in a domain dramatically affect its value, and serious domain investors study letter frequency data carefully.

Domain investors categorize letters into tiers. The premium letters — the most frequent and desirable — include common consonants and vowels that appear in everyday English words. The least desirable letters are Q, X, Z, and J. A middle tier includes letters that appear with moderate frequency.

When buying four-letter domains, getting premium letters costs more, but that premium is the price of quality. A domain made of four premium letters is pronounceable, memorable, and has far more potential end users than a random string containing Q and Z.

The specific valuations of letter combinations are something experienced domainers study extensively. Large portfolio holders maintain databases tracking which users bid on which names, what prices cleared at auction, and how letter combinations correlate with sale prices. Building and maintaining this kind of dataset is part of the work that separates serious investors from casual speculators.

Price History Around the Buyout

Historical auction data from the months surrounding the November 2007 buyout illustrates how the market priced these domains in real time.

A year before the buyout, premium-letter four-letter .coms were selling for around $60 at auction. Even a few months before the buyout, with the available supply clearly dwindling, prices remained near the minimum bid. Investors still had doubts. When more domains dropped (expired and became available), confidence wavered — people worried that something was wrong with the thesis.

By September 2007, prices started climbing meaningfully. Buyers had to pay $100 or more for good names, though occasional bargains still appeared. By October, the land rush was underway and prices climbed further. On and around November 2, the buyout date, premium-letter domains were trading near $200.

After the initial spike, prices settled back somewhat. By 2008, premium four-letter .coms were trading around $170. The financial crisis of 2008 affected domain values along with every other asset class, but the market recovered faster than many expected.

Mid-tier domains — those with one or two less desirable letters — followed the same trajectory at lower price points. A domain with three premium letters and one mid-tier letter might have traded at $59 near the buyout date while an all-premium combination reached $200.

Doing Your Homework

Successful domain investing requires data, not gut instinct. The most important step is studying the major buyers — the people and companies who consistently acquire domains at auction. By dumping historical auction data into a database and sorting by buyer, patterns emerge. You begin to see who the informed buyers are, what they pay, and which types of names they target.

This research serves another purpose: finding your community. Through auction data analysis, it becomes possible to identify competitors, reach out, and build relationships. Several successful domainers have found real-life friends and support networks through this process. That support network matters because domain investing requires patience and conviction. Without people to discuss strategy with — especially during periods when the market dips and confidence wavers — it is easy to sell too early or lose nerve entirely.

Selling: Domainer-to-Domainer vs. End User

There are two ways to sell a domain: to another domainer, or to an end user (a business that will actually use the domain).

Domainer-to-domainer sales are efficient. The market between professional investors is well-informed, so price variation is small and the reward relative to time spent is low. Most large portfolio holders avoid this kind of trading except for short-term tactical reasons.

The real money is in end-user sales. This market is inefficient — a business that needs a specific domain for its brand will pay a significant premium over what another domainer would offer. The challenge is timing. If you own one domain, you might wait 20 years for an end-user buyer. If you own 20 domains, statistical probability suggests you might see one end-user sale per year. The reward is high, but only for those willing to hold for the long term.

Legal Considerations

Internet transactions are relatively inexpensive, and the legal framework is correspondingly lightweight. The primary legal mechanism in domain disputes is the Uniform Domain-Name Dispute-Resolution Policy (UDRP). A complainant can file a UDRP case for approximately $1,500, but they must prove three elements — that the domain is identical or confusingly similar to their trademark, that the registrant has no legitimate interest in the domain, and that the domain was registered and used in bad faith.

All three elements must be proven. This standard protects legitimate domain investors from having their names seized by trademark holders who simply want a convenient domain.

An important counter-mechanism exists called reverse domain name hijacking. When a trademark holder files a frivolous UDRP complaint — knowing they cannot meet the three-element test but hoping to intimidate the domain owner into giving up the name — the panel can find reverse domain name hijacking. This finding goes on the complainant’s record and serves as a deterrent against abusive filings.

Key Takeaways

This case study is not investment advice — it illustrates how supply-and-demand principles apply to a specific digital asset class. The core observations:

- Supply is permanently fixed — 456,976 four-letter .coms can ever exist, and the buyout proved that demand can absorb the entire supply

- Letter quality determines value — premium letters command premiums for good reason

- Data beats intuition — successful investors maintain databases, study auction results, and build analytical frameworks

- End-user sales drive returns — the inefficient market between domains and businesses is where real value is captured

- Patience is non-negotiable — domain investing is a long-term hold strategy, not a quick flip

- Community matters — finding other serious investors to discuss strategy with provides both information and psychological support during market uncertainty